[With Calculators] Budgeting, Investing, Loan & Retirement Rules That You Should Know 2026

![[With Calculators] Budgeting, Investing, Loan & Retirement Rules That You Should Know 2026 | Representative Image](https://heroxrohit.in/wp-content/uploads/2026/03/With-Calculators-Budgeting-Investing-Loan-Retirement-Rules-That-You-Should-Know-2026.webp)

[With Calculators] Budgeting, Investing, Loan & Retirement Rules That You Should Know 2026 | Representative Image

Aaj kal personal finance samjun ghene khup confusing zala aahe. Social media var pratyek jan vegla advice deto ani pratyek rule perfect watto. Pan 2026 madhe reality thodi vegli aahe. Inflation high aahe. Rent ani daily expenses fast vadhat aahet. Salary growth itki fast nahiye. Mhanun purane rules blindly follow karne ata smart nahiye.

Khara point asa aahe ki rules change zalele nahiye, pan tyacha use karaychi paddhat change zali aahe. Jo formula 2018 madhe kaam karto hota, to aaj exact same kaam karil asa nahi. Tumhala tyala tumchya income, lifestyle ani goals pramane adjust karava lagel.

Jar tumhala paisa control karaycha asel, stress kami karaycha asel ani future secure karaycha asel, tar tumhala updated ani practical system pahije. Ya article madhe tumhala budgeting, investing, debt management ani retirement planning cha complete India-focused blueprint milnar aahe. He theory nahiye. He real life madhe kaam karanare rules aahet.

Table of Contents

Key Takeaways

- 50/30/20 rule ata flexible zala aahe ani tumchya situation pramane change karava lagto

- Rule of 72 ani SIP discipline long term wealth build karayla khup powerful aahe

- 40 percent EMI rule follow nahi kela tar financial stress nischit aahe

- 4 percent rule India sathi safe nahiye, 3 te 3.5 percent jast realistic aahe

- Personalisation ha saglyat motha rule aahe, copy paste strategy fail hote

All Personal Finance Rules in One Table (2026 India)

| Category | Rule Name | Mathematical Formula / Logic | Core Purpose |

|---|---|---|---|

| Budgeting | 50/30/20 Rule | 50% Needs, 30% Wants, 20% Savings | Balanced monthly spending |

| 70/20/10 Rule | 70% Spending, 20% Saving, 10% Debt | Debt heavy situation control | |

| 3-6 Month Rule | Monthly Expenses × 3 or 6 | Emergency fund build karne | |

| 24 Hour Rule | 24 hours wait before spending | Impulse control | |

| Investing | Rule of 72 | 72 ÷ Return = Double time | Compounding samjun ghene |

| 100 Minus Age | 100 – Age = Equity % | Asset allocation | |

| Rule of 114 | 114 ÷ Return = Triple time | Long term growth | |

| 10-5-3 Rule | 10% Equity, 5% Debt, 3% Cash | Realistic returns | |

| Loans & Debt | 40% EMI Rule | EMI < 40% income | Debt control |

| 2x Purchase Rule | Price × 2 < Cash | Luxury control | |

| Debt Avalanche | High interest first | Interest save karne | |

| 20/4/10 Rule | 20% down, 4 year loan, 10% income | Smart car buying | |

| Retirement | 4% Rule | Portfolio × 0.04 | Withdrawal planning |

| 25x Rule | Expenses × 25 | Retirement corpus | |

| 10x Income Rule | Income × 10 | Life insurance | |

| 80% Rule | Income × 0.80 | Retirement income |

1. Budgeting Rules Explained (Example + Benefits)

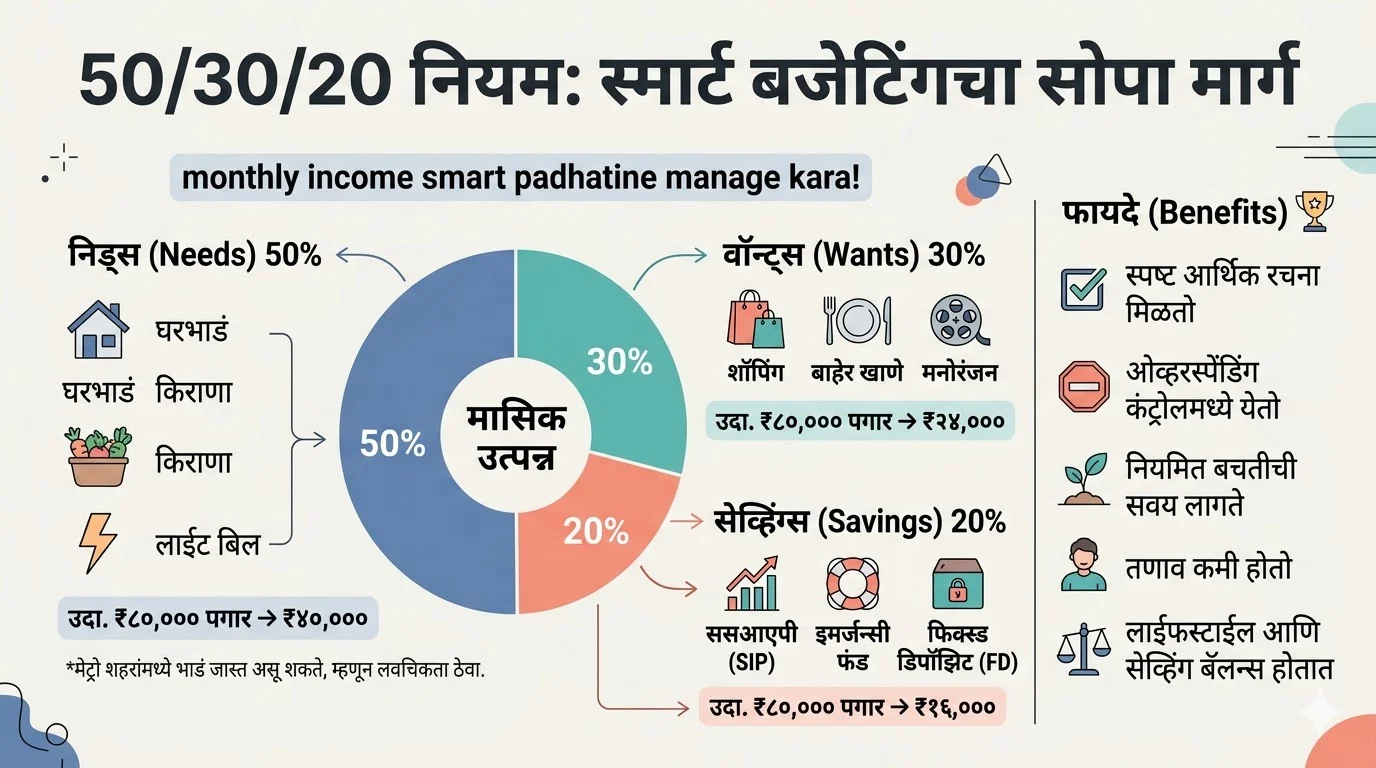

1) 50/30/20 Rule

50/30/20 rule ha ek simple pan powerful budgeting framework aahe jo tumhala tumcha monthly income smart padhatine manage karayla madat karto. Ya rule pramane tumcha income teen parts madhe divide karto: 50 percent needs (basic expenses), 30 percent wants (lifestyle expenses) ani 20 percent savings (future sathi investment ani emergency fund). He rule especially beginners sathi khup useful aahe karan he overthinking kami karto ani clear structure deto.

Example: Salary ₹80,000

Needs = ₹40,000 (rent, groceries, bills)

Wants = ₹24,000 (shopping, eating out, entertainment)

Savings = ₹16,000 (SIP, emergency fund, FD)

Samja tumhi ha rule follow kela tar tumhala pratyek rupee cha direction kalto. Tumhi overspending karat nahi ani saving pan consistent rahte. Pan metro cities madhe rent jast aslyamule needs 50% peksha jast jau shaktat, mhanun thoda flexible approach thevne important aahe.

Benefits:

- Clear financial structure milto

- Overspending control madhe yeto

- Regular saving habit develop hote

- Stress kami hoto karan planning clear aste

- Lifestyle ani saving donhi balance hotat

Help: Ha rule tumhala financial discipline build karayla madat karto. Jar tumhi navin asal tar ha best starting point aahe. Nantar tumhi tumchya income ani goals pramane percentages adjust karu shakta.

Use Tool: 50 30 20 Rule Calculator

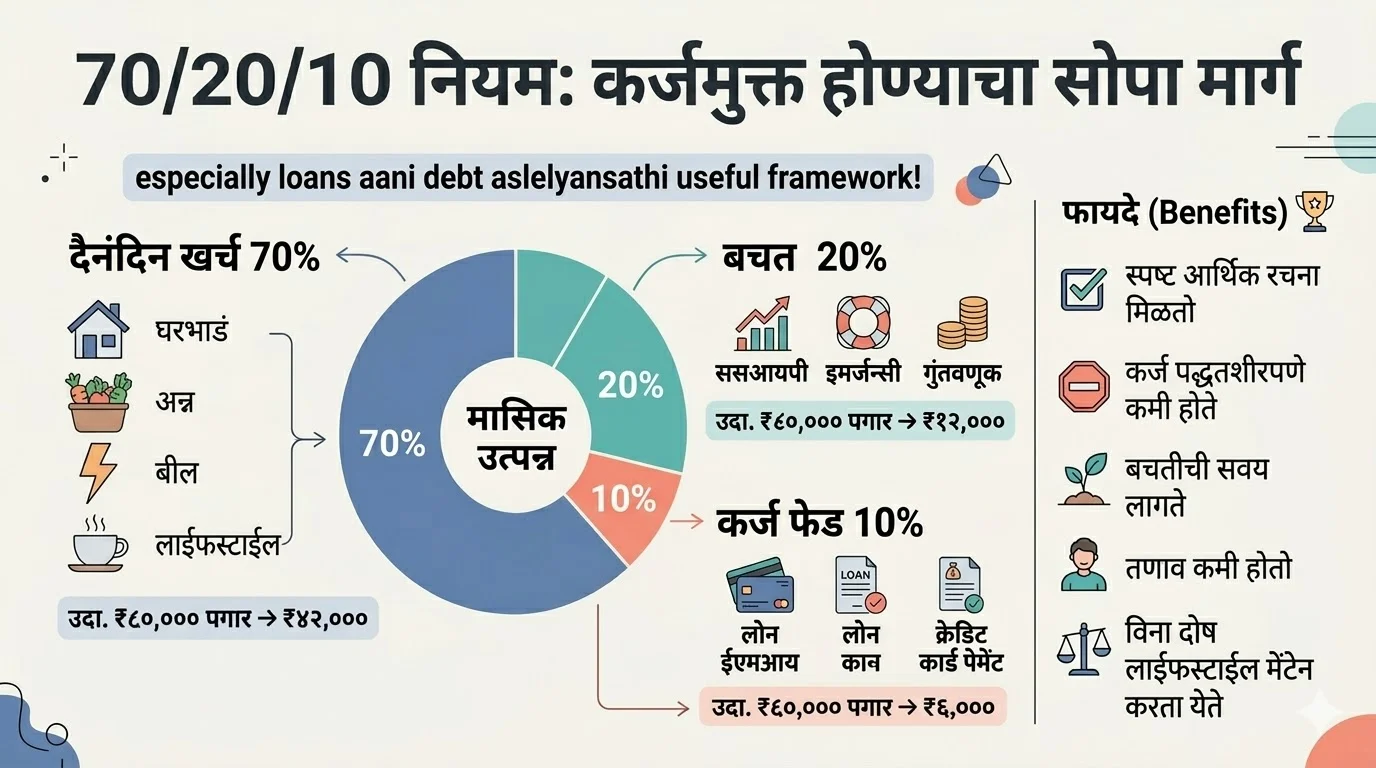

2) 70/20/10 Rule

70/20/10 rule ha ek simple pan powerful budgeting framework aahe jo especially tyanchya sathi useful aahe jyancha kade already loan kiwa debt aahe. Ya rule madhe tumcha monthly income teen parts madhe divide kela jato: 70 percent daily spending sathi, 20 percent saving sathi ani 10 percent debt repayment sathi. He structure tumhala ek clear direction deto ki paisa kasa manage karaycha.

Example: Salary ₹60,000

Spending = ₹42,000 (rent, food, bills, lifestyle)

Saving = ₹12,000 (SIP, emergency fund, investments)

Debt = ₹6,000 (loan EMI, credit card payment)

Ya rule cha main advantage asa aahe ki tumhi ekach veles teen important goshti manage karta: lifestyle, future ani debt. Barech lok saving karaycha try kartat pan debt ignore kartat, kiwa sagla paisa debt madhe taktat ani saving nahi kart. 70/20/10 rule he balance maintain karto.

Benefits:

- Clear structure milto, confusion kami hoto

- Debt systematically reduce hoto

- Saving habit develop hote

- Financial stress kami hoto

- Lifestyle maintain karta yeto without guilt

He rule especially tyanchya sathi best aahe jyancha kade personal loan, credit card balance kiwa EMI aahe. Jar tumhi ha rule consistently follow kela, tar tumhi halu halu debt free hou shakta ani tyach veles savings pan build karu shakta.

Help: He rule tumhala discipline deto ani tumcha paisa control madhe thevto. Long term madhe he tumhala financial stability ani peace of mind deto.

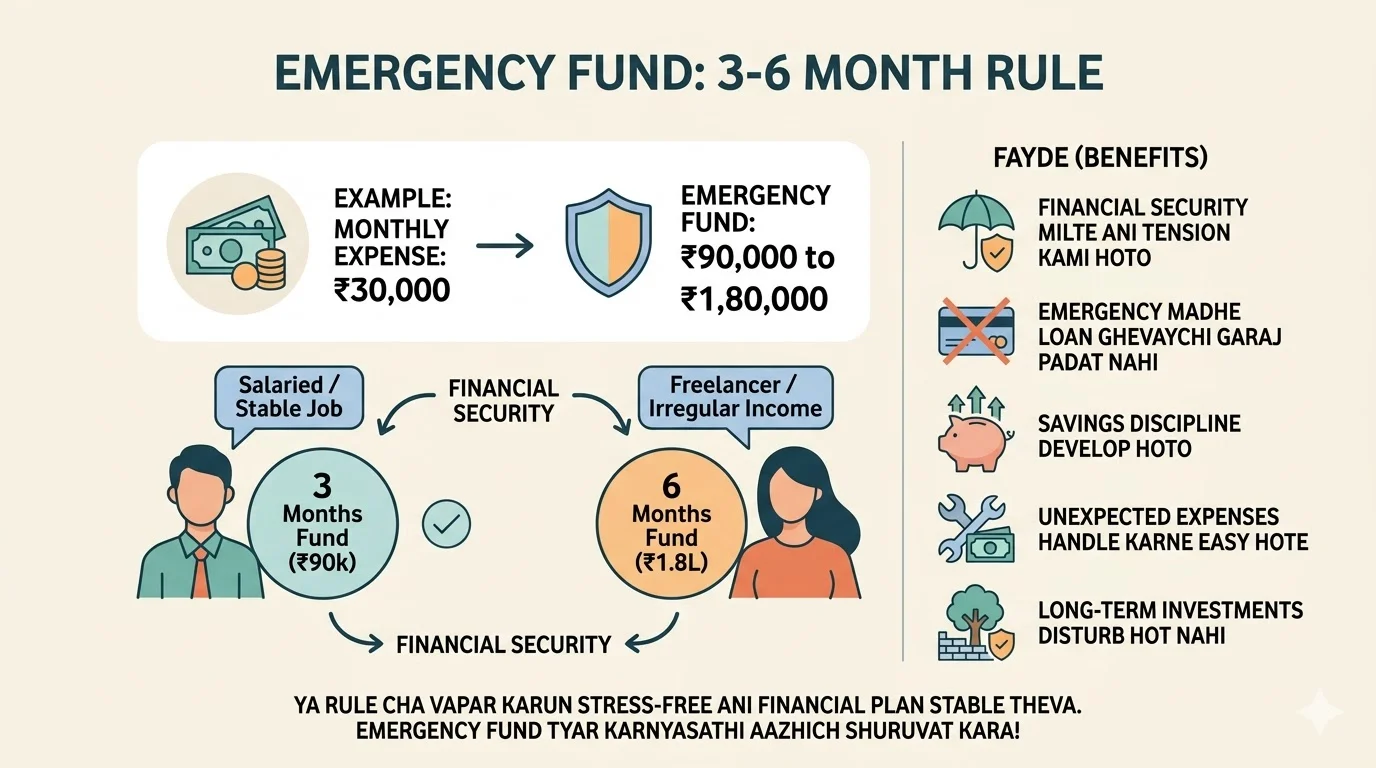

3) 3-6 Month Rule

Example: Monthly expense ₹30,000

Emergency fund = ₹90,000 te ₹1,80,000

Explanation: 3-6 Month Rule ha ek simple pan khup powerful financial tool aahe jo tumhala unexpected situations madhe protect karto. Ya rule nusar tumhi tumchya monthly expenses cha kamit kami 3 te 6 pat amount side la thevaycha asto. He paisa tumhi savings account, liquid fund kiwa FD madhe thevu shakta jithe te easily access karta yeto.

Samja tumcha monthly expense ₹30,000 aahe, tar tumhala ₹90,000 te ₹1,80,000 emergency fund build karava lagel. Jar tumhi salaried aahet ani job stable aahe tar 3 months enough asu shakto. Pan jar tumhi freelancer aahet kiwa income irregular aahe tar 6 months fund jast safe aahe.

He tool tumhala financial shocks pasun vachavto jase ki job loss, medical emergency, sudden repair expenses kiwa family emergency. Jar emergency fund nasel tar lok credit card kiwa personal loan gheun problem solve kartat, jyamule debt vadhato.

Benefits:

- Financial security milte ani tension kami hoto

- Emergency madhe loan ghevaychi garaj padat nahi

- Savings discipline develop hoto

- Unexpected expenses handle karne easy hote

- Long term investments disturb hot nahi

Help: He rule follow kela tar tumhi stress free rahu shakta ani tumcha financial plan stable rahato. Emergency fund mule tumhala confidence milto ki kahi pan situation madhe tumhi financially ready aahet.

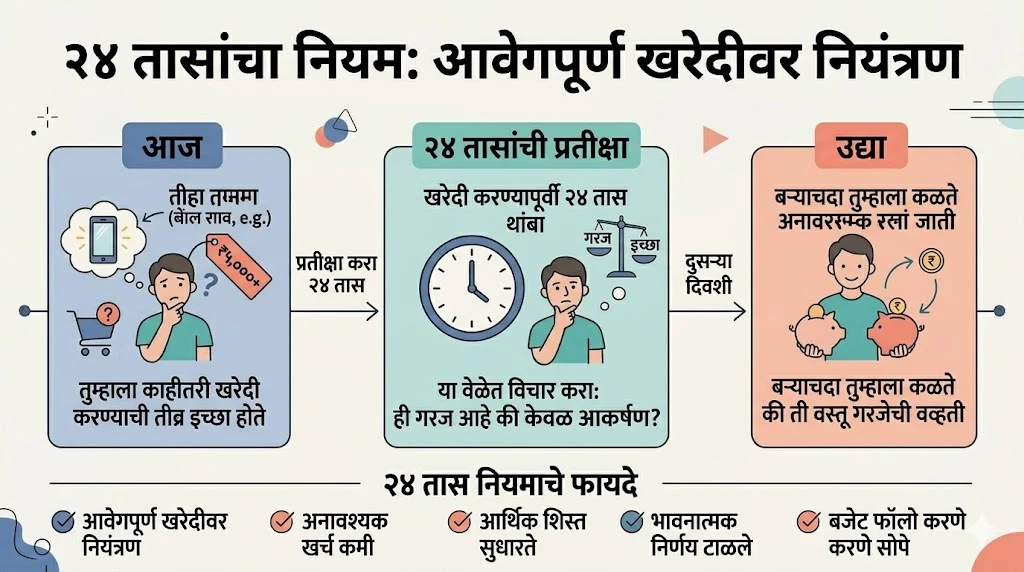

4) 24 Hour Rule

Samja tumhala ₹5,000 cha gadget online disla ani tumhala to turant ghaycha aahe asa vatla. Ya situation madhe 24 Hour Rule apply kara. Mhanje tumhi turant purchase karu naka, pan 24 hours wait kara. Ya 24 hours madhe tumhi vichar kara ki ha kharcha kharach garjecha aahe ka, ki fakt momentary excitement mule decision ghetay.

Dusrya divshi jar tumhala to gadget tevadhach important vatla, tar tumhi to gheu shakta. Pan bahutek vela asa hota ki 24 hours nantar interest kami hoto ani tumhala kalta ki ha kharcha avoid karta yeto.

Benefit:

- Impulse buying control madhe yeto

- Unnecessary kharcha kami hoto

- Financial discipline improve hoto

- Emotional decision ghetnyapasun vachavto

- Budget follow karne easy hote

Help:

- Tumhala conscious spending chi habit lagte

- Savings automatically vadhte karan random kharcha kami hoto

- Long term madhe paisa invest karayla jast milto

- Financial stress kami hoto

- Smart decision making develop hote

He rule simple aahe pan khup powerful aahe. Jar tumhi ha daily life madhe apply kela, tar tumcha spending pattern completely change hoil ani tumhi jast responsible financial decisions gheu shakal.

2. Investing Rules Explained (Example + Benefits)

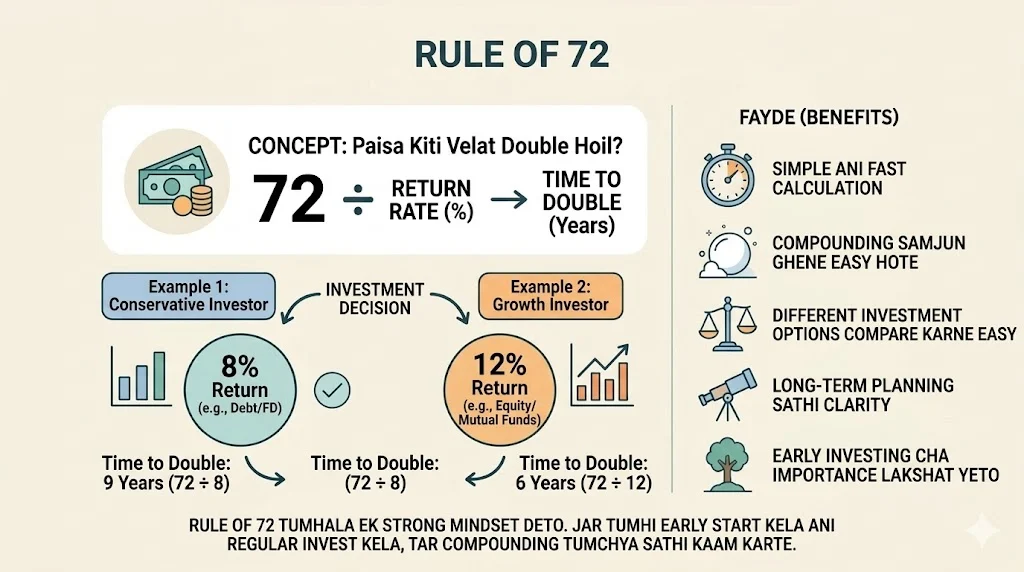

1) Rule of 72

Rule of 72 ha ek simple pan powerful financial tool aahe jo tumhala investment kiti velat double hoil he quickly calculate karayla madat karto. Formula khup easy aahe: 72 la tumcha expected annual return rate ne divide kara. Jo answer yeil, to tumcha paisa double honyasathi laganara approximate time asto.

Example:

Samja tumhi ek investment keli jithe average return 8 percent aahe. 72 ÷ 8 = 9 years

Mhanje tumcha paisa roughly 9 varshat double hoil.

He rule exact nahiye pan quick estimation sathi khup useful aahe, especially beginners sathi. Tumhala compounding cha real effect samjun ghaycha asel tar ha best starting point aahe.

Benefits:

- Simple ani fast calculation – calculator kiwa complex formula chi garaj nahi

- Compounding samjun ghene easy hote

- Different investment options compare karayla madat karto

- Long term planning sathi clarity milte

- Early investing cha importance lakshat yeto

Help:

Rule of 72 tumhala ek strong mindset deto ki wealth build karayla time lagto pan consistency mule result milto. Jar tumhi early start kela ani regular invest kela, tar compounding tumchya sathi kaam karte. He rule tumhala patience develop karayla madat karto ani short term market fluctuations ignore karayla shikavto.

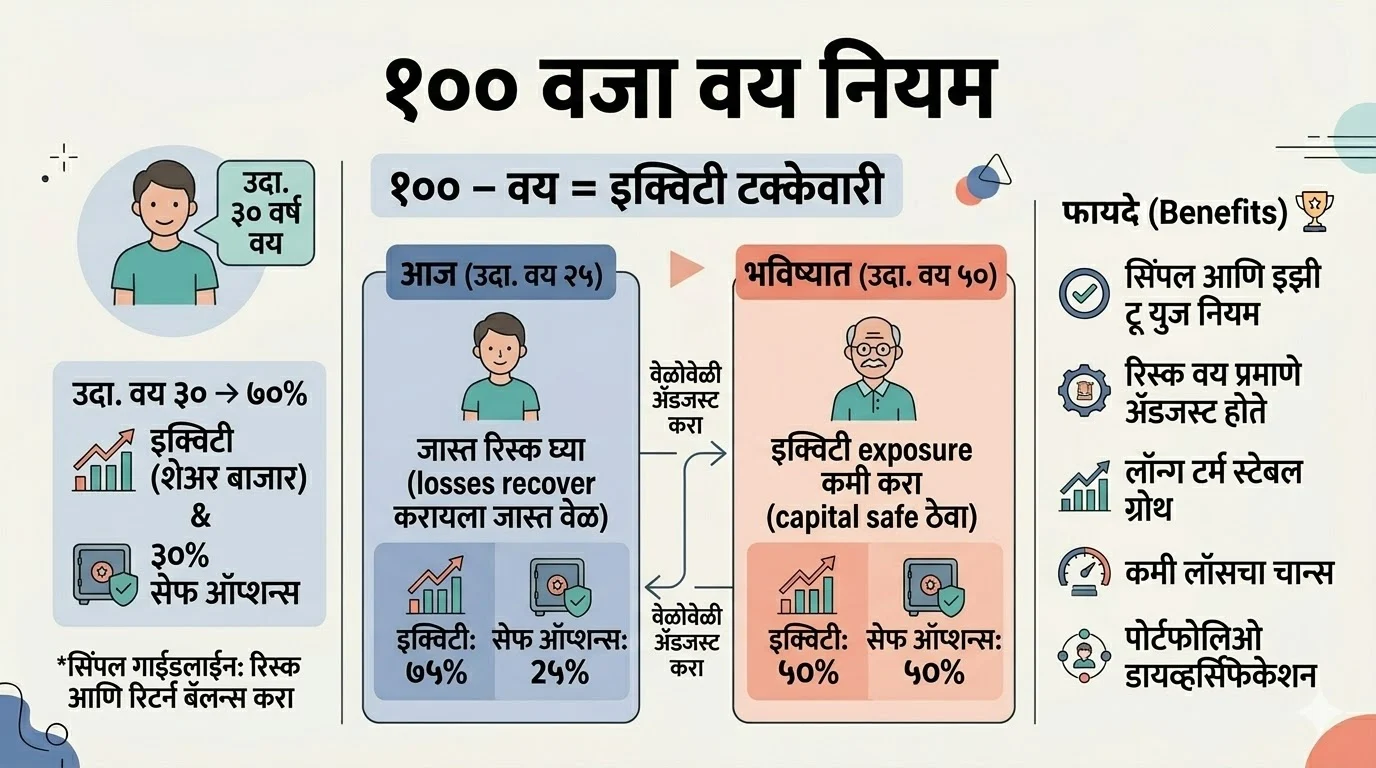

2) 100 Minus Age Rule

Example: Samja tumcha age 30 aahe. 100 minus 30 = 70, mhanje tumhi tumcha investment cha 70 percent equity madhe thevu shakta ani urlela 30 percent safer options jase debt funds kiwa fixed income madhe thevu shakta. He ek simple guideline aahe je tumhala tumcha risk ani return balance karayla madat karto.

He tool mhanje 100 Minus Age Rule, jo ek basic asset allocation framework aahe. Yacha main purpose asa aahe ki tumhi tumcha age pramane investment risk adjust kara. Jast young asal tar jast risk gheu shakta karan tumchya kade time jast aahe losses recover karayla. Jase jase age vadhte, tase equity exposure kami karun safer investments madhe shift karaycha.

Example sathi, jar tumhi 25 varshache asal tar 75 percent equity thevu shakta. Pan jar tumhi 50 varshache asal tar 50 percent equity ani 50 percent debt thevne safer rahte. He tumhala market volatility pasun protect karto ani retirement javal aalyavar capital safe thevayla madat karto.

Benefits:

- Simple ani easy to use rule aahe, konihi follow karu shakto

- Risk automatically age pramane adjust hoto

- Long term madhe stable growth milte

- Market crash madhe full loss honyachi chance kami hote

- Portfolio diversification maintain rahte

He rule beginners sathi khup useful aahe karan tyanna complex planning karaychi garaj nahi. Pan he ek starting point aahe, final decision tumcha goals, income ani risk tolerance var depend karto.

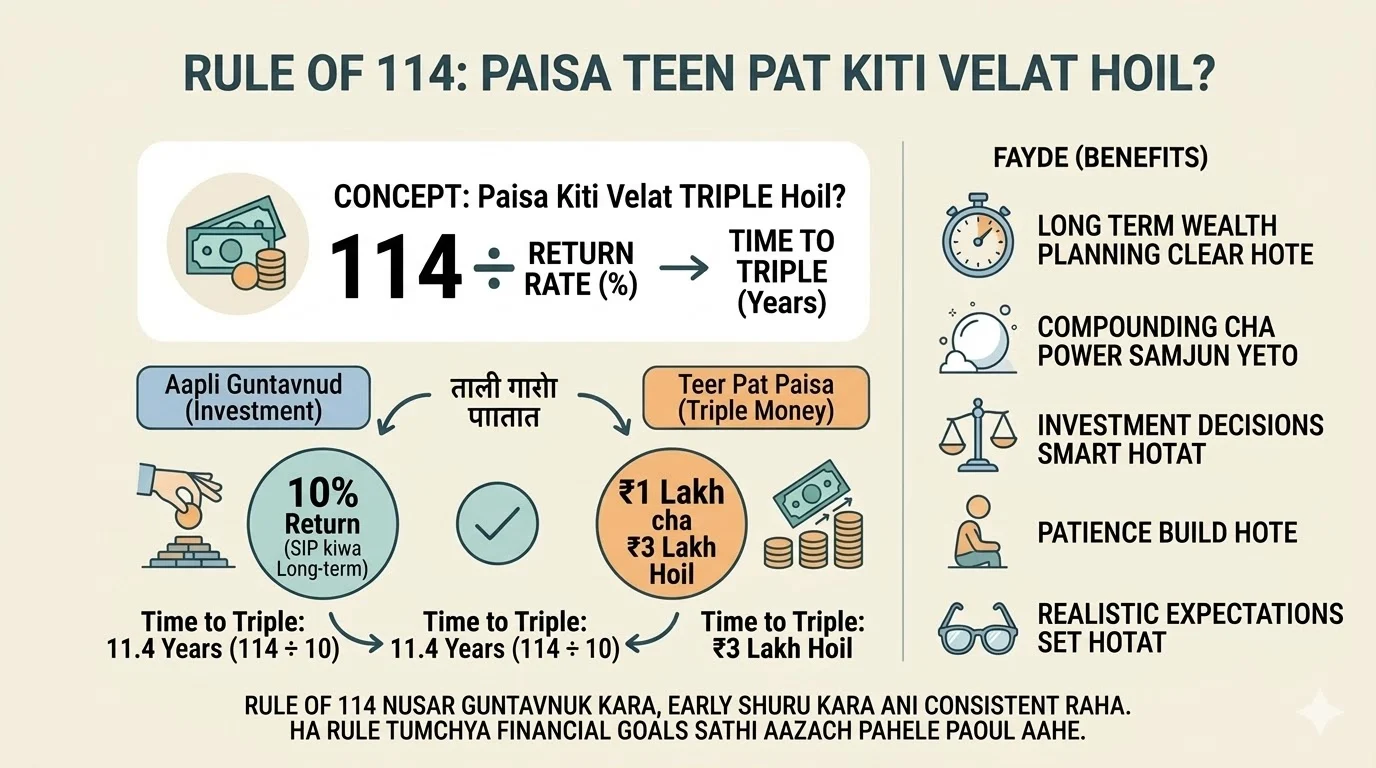

3) Rule of 114

Example: Samja tumhi ₹1 lakh invest karta ani tumhala 10 percent annual return milto. Rule of 114 nusar:

114 ÷ 10 = 11.4 years

Mhanje tumcha paisa approx 11.4 varshat triple hoil, mhanje ₹1 lakh cha ₹3 lakh hoil.

Explanation: Rule of 114 ha ek simple mental shortcut aahe jo tumhala sangto ki tumcha investment kiti velat 3 pat hoil. He especially long term investors sathi khup useful aahe karan te compounding cha real effect samjun gheu shaktat. Jast return asel tar paisa fast triple hoto, ani kami return asel tar jast vel lagto.

Benefits:

- Long term wealth planning clear hote

- Compounding cha power samjun yeto

- Investment decisions smart hotat

- Patience build hote

- Realistic expectations set hotat

Help: He rule tumhala motivate karto ki tumhi early invest kara ani consistent raha. Jar tumhi SIP kiwa long term investment karta, tar tumhala kalte ki time ani return donhi important aahet. Yane tumhi better financial goals set karu shakta ani future sathi strong planning karu shakta.

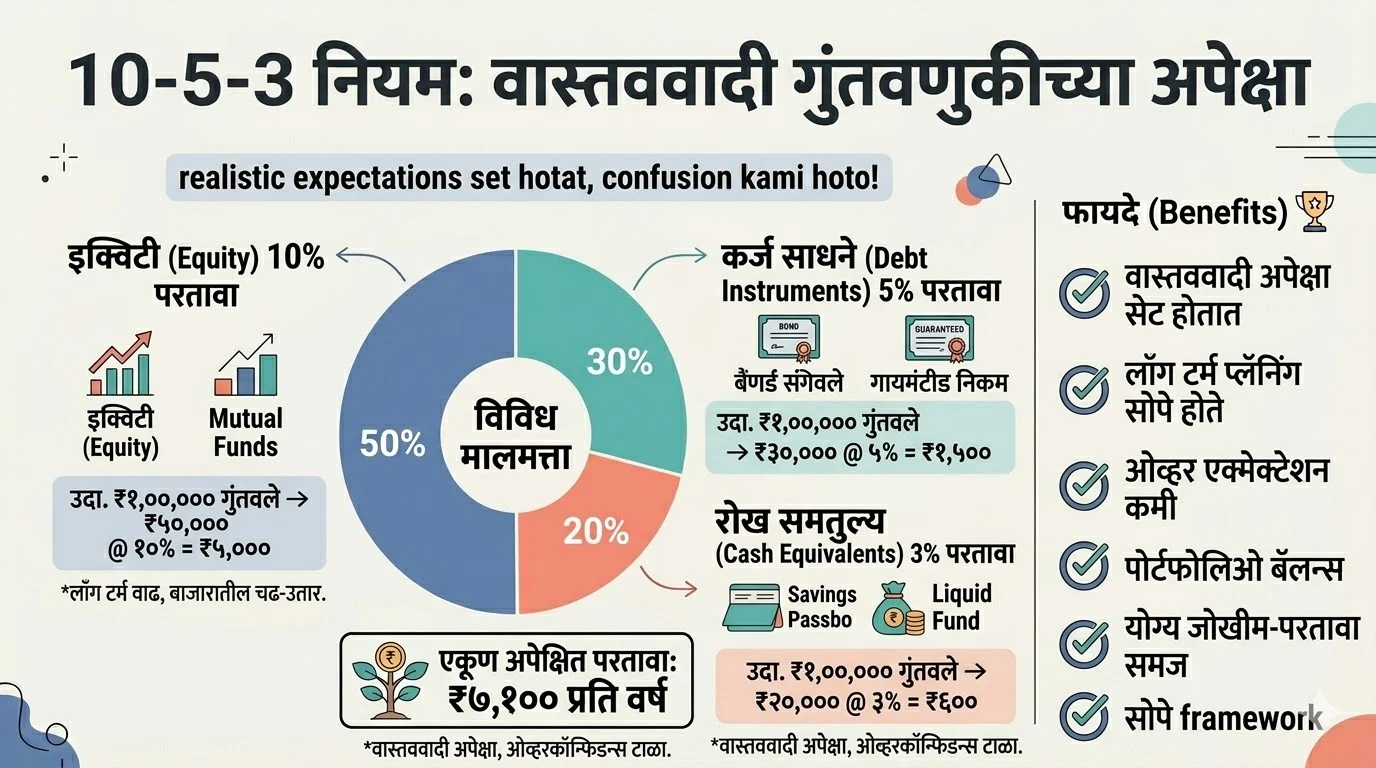

4) 10-5-3 Rule

10-5-3 rule ha ek simple pan powerful guideline aahe jo tumhala realistic investment expectations set karayla madat karto. Ya rule nusar, long term madhe tumhi vegveglya asset classes madhun approximate returns expect karu shakta.

Equity investments (jase stocks kiwa equity mutual funds) sathi around 10 percent return, debt instruments (jase bonds kiwa fixed income funds) sathi 5 percent return, ani cash equivalents (jase savings account kiwa liquid funds) sathi 3 percent return consider kele jatat.

Example: Samja tumhi ₹1,00,000 invest kartay ani tumcha portfolio asa divide aahe:

Equity = ₹50,000 → 10% return = ₹5,000

Debt = ₹30,000 → 5% return = ₹1,500

Cash = ₹20,000 → 3% return = ₹600

Total expected return = ₹7,100 per year. He ek realistic expectation aahe jo tumhala overconfidence kiwa unrealistic planning pasun vachavto.

Benefits:

- Realistic expectations set hotat, jyamule tumhi market madhe panic hot nahi

- Long term planning easy hote karan tumhala approximate returns mahit astat

- Over expectation kami hotat, jyamule wrong investment decisions talta yetat

- Portfolio balance maintain karayla madat hote

- Risk ani return cha proper understanding develop hoto

- Beginners sathi simple ani easy to follow framework aahe

Help: Ha rule tumhala discipline deto ani tumcha focus long term growth var thevto. Market madhe short term fluctuations astat, pan jar tumhi ya rule pramane expectations set kele tar tumhi emotional decisions ghetnar nahi. He especially tyanchya sathi useful aahe je navin investing suru kartat ani jyan na realistic planning karaychi aahe.

3. Loan & Debt Rules Explained (Example + Benefits)

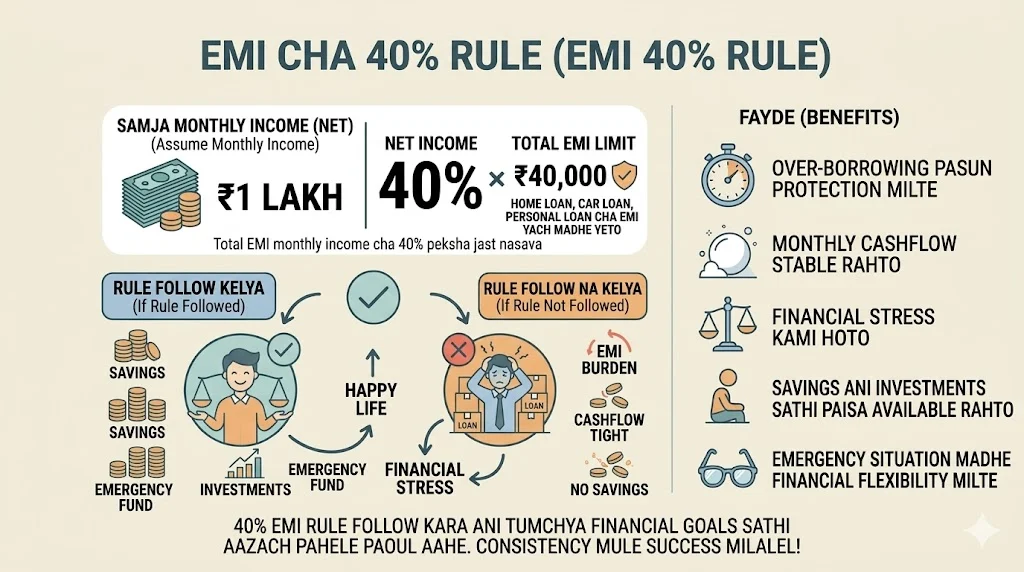

1) 40% EMI Rule

40% EMI Rule ha ek simple pan powerful guideline aahe jo tumhala sangto ki tumcha total EMI (home loan, car loan, personal loan, credit card payments) tumchya monthly income cha 40% peksha jast nasava. Ha rule tumcha financial balance maintain karayla madat karto ani over-borrowing pasun vachavto.

Example:

Samja tumchi monthly salary ₹1 lakh aahe. Tar tumcha total EMI ₹40,000 peksha jast nasava. Jar tumhi ₹50,000 EMI bharat asal, tar tumcha cashflow tight hoil ani daily expenses manage karne difficult hoil.

Ha rule especially important aahe karan aaj kal easy loans mule lok jast borrowing kartat ani nantar stress madhe yetat. 40% limit follow keli tar tumhala savings, investments ani emergency sathi pan paisa rahato.

Benefits:

- Over borrowing pasun protection milte, mhanje tumhi unnecessary loan ghetnar nahi

- Monthly cashflow stable rahto, jyamule daily expenses smoothly manage hotat

- Financial stress kami hoto, karan EMI burden control madhe rahto

- Savings ani investments sathi paisa available rahto

- Emergency situation madhe financial flexibility milte

Ha rule follow karun tumhi long term madhe financially secure rahu shakta ani debt trap madhe padnyapasun vachu shakta.

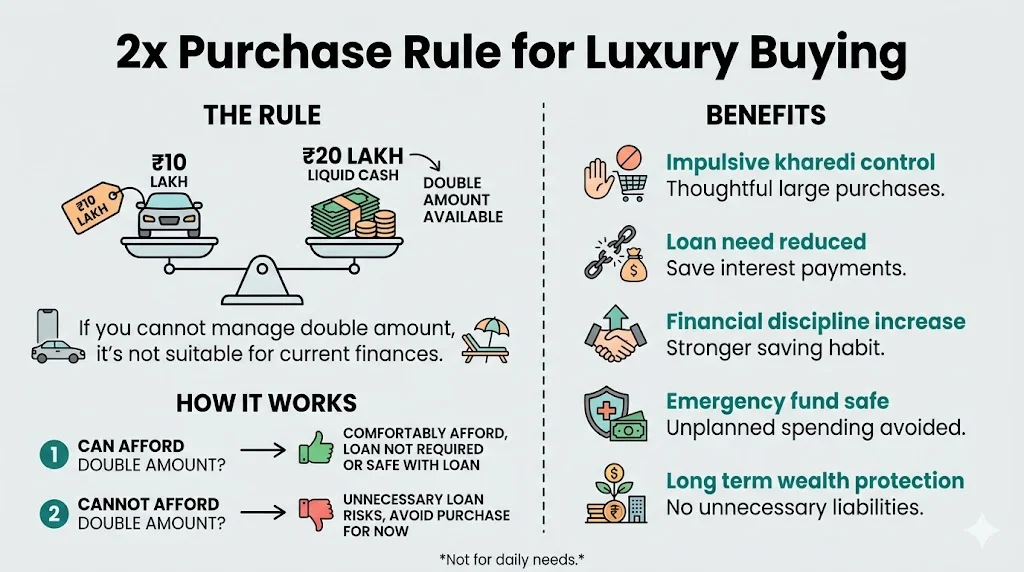

2) 2x Purchase Rule

Ha rule luxury kharedi sathi ek powerful decision-making tool aahe jo tumhala financial stress pasun vachavto. Simple logic asa aahe ki jar tumhi kahi expensive vastu ghetoy, tar tumchya kade tyacha double amount cash asla pahije. Mhanje tumhi fakt afford nahi kart, tar comfortably afford kart aahat.

He rule tumhala ek strong filter deto. Jar tumhi double amount manage karu shakat nahi, tar samja ki ti vastu tumchya current financial situation sathi suitable nahi. He tumhala unnecessary loan ghetnyapasun ani future stress pasun vachavto.

Example: Samja tumhala ₹10 lakh chi car ghaychi aahe. Ya rule pramane tumchya kade kamit kami ₹20 lakh liquid cash asla pahije. Jar tumchya kade fakt ₹10-12 lakh aahet ani baki loan gheun car ghetli, tar tumhi risk gheta aahat. Pan jar ₹20 lakh aahet, tar tumhi loan gheun pan safe aahat kiwa full cash madhe pan gheu shakta.

He rule especially luxury items sathi use hoto jase car, gadgets, vacations kiwa high-end lifestyle kharcha. He daily needs sathi nahiye.

Benefits:

- Impulsive kharedi control hote karan tumhi pratyek mothya kharedi purvi vichar karta

- Loan ghetnyachi garaj kami hote ani interest madhe paisa vachto

- Financial discipline vadhte ani saving habit strong hote

- Emergency fund disturb hot nahi karan tumhi planned kharcha karta

- Long term wealth protect hote karan unnecessary liabilities avoid hotat

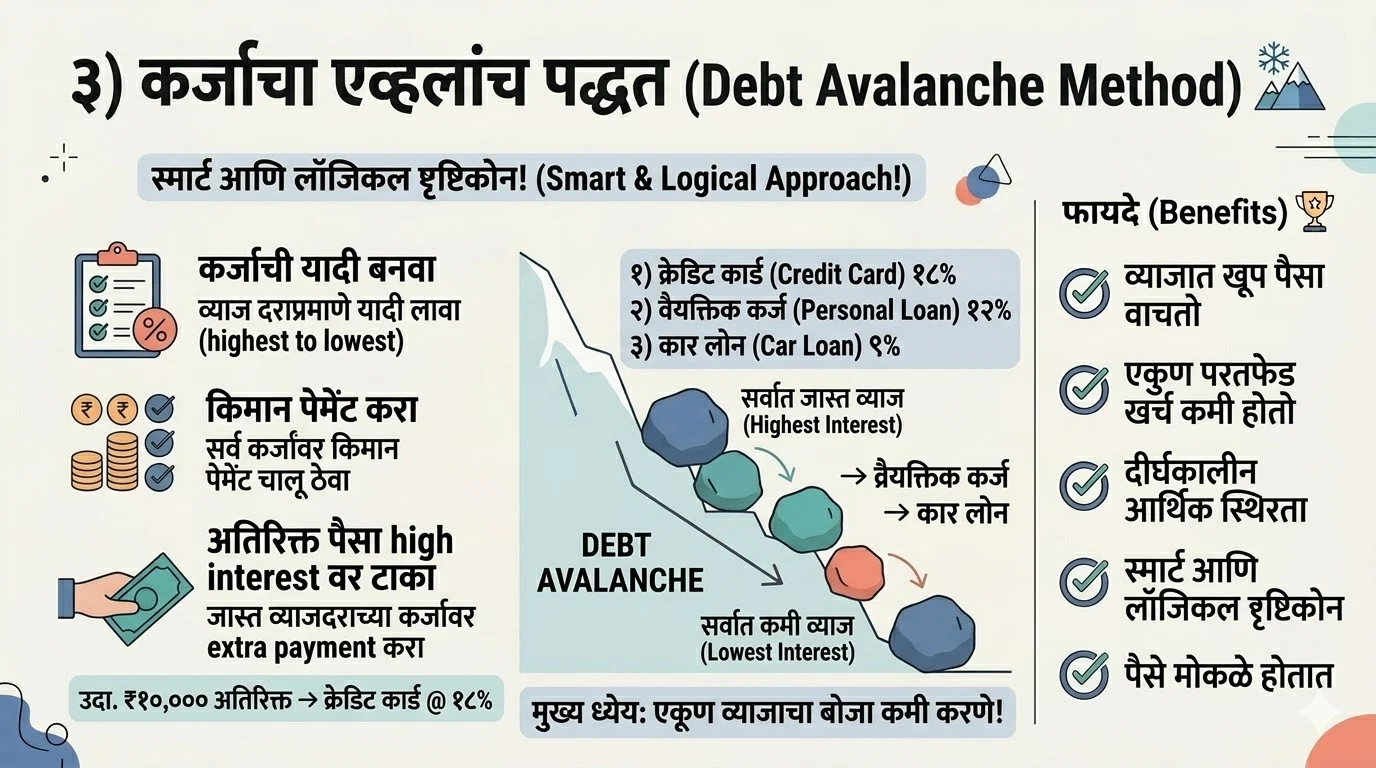

3) Debt Avalanche Method

Ya method madhe tumhi saglyat jast interest rate aslela loan pahile close karta, jyala Debt Avalanche method mhantat. He ek smart ani logical approach aahe jithe tumhi tumcha total interest burden kami karaycha focus karta. Ya method madhe tumhi sagle loans list karta ani tyanna interest rate pramane arrange karta, highest to lowest. Nantar tumhi minimum payment saglya loans var karta, pan extra paisa highest interest loan var takta.

Example: Samja tumchya kade 3 loans aahet: Credit card 18%, personal loan 12%, ani car loan 9%.

Ya case madhe tumhi saglyat pahile credit card var extra payment karal, karan tyacha interest jast aahe. Credit card close zala ki tumhi next personal loan var focus karal, ani nantar car loan.

He method thoda patience demand karto, pan long term madhe khup effective aahe. Tumhala suruvatila fast results disnar nahi, pan interest saving mule tumcha total repayment amount significantly kami hoto.

Benefits:

- Interest madhe khup paisa vachto, karan high interest loan pahile close hoto

- Total debt repayment cost kami hote

- Long term madhe financial stability vadhte

- Smart ani logical approach mule better control milto

- Faster wealth building sathi paisa free hoto

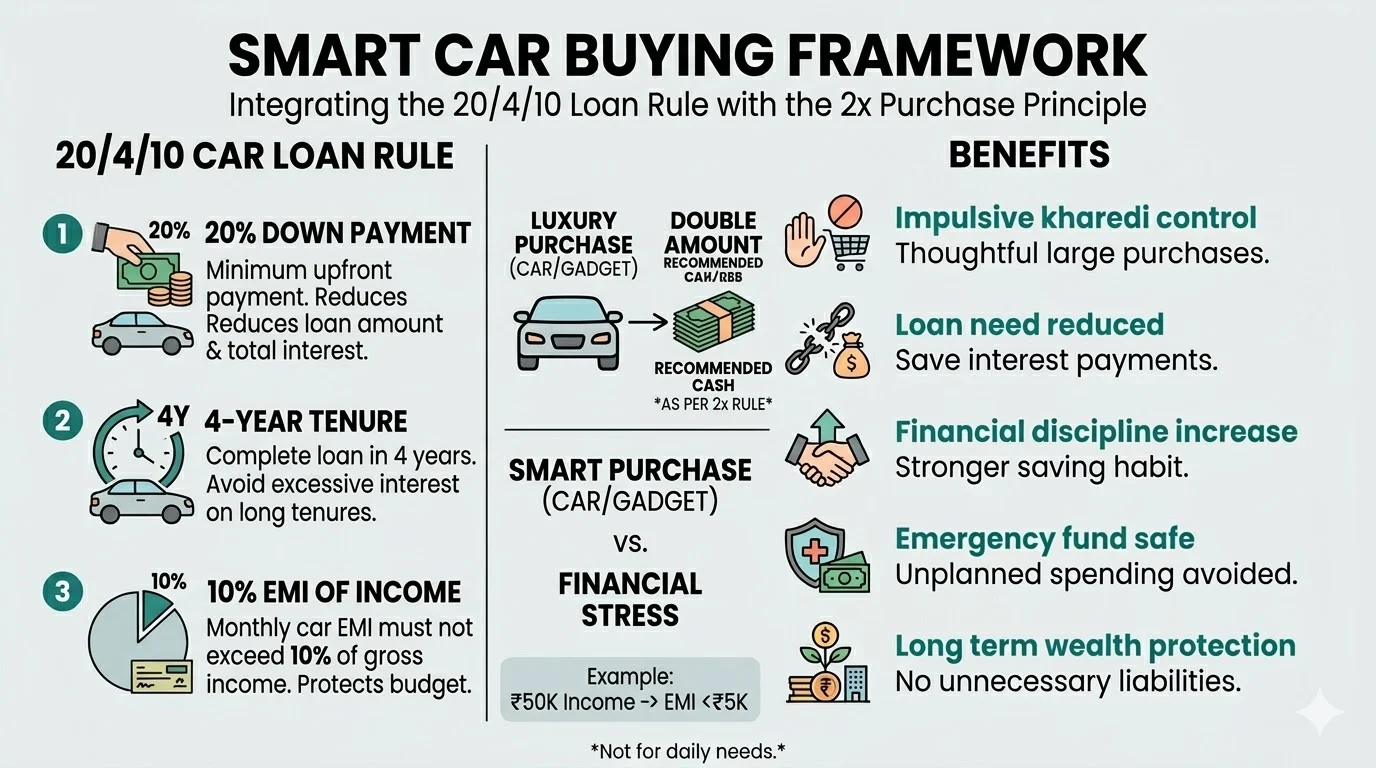

4) 20/4/10 Rule

Ha rule mainly car loan sathi use hoto ani smart financial decision ghyayla madat karto. 20/4/10 rule mhanje ek simple framework aahe jo tumhala car kharedi kartana over spending pasun vachavto ani long term financial stress kami karto.

Logic asa aahe:

- 20% down payment: Car cha total price madhun kamit kami 20% tumhi upfront bharava. Yane loan amount kami hoto ani interest pan kami lagto.

- Loan tenure 4 years: Loan 4 varshat complete karaycha. Jast tenure asel tar EMI kami disel pan total interest jast bharava lagto.

- EMI income cha 10% peksha jast nasava: Tumcha monthly income cha 10% peksha jast EMI nasava, mhanje tumcha budget disturb hot nahi.

Example bagha: Jar tumcha monthly salary ₹50,000 aahe, tar tumcha EMI ₹5,000 chya aat asava. Samja tumhi ₹6 lakh chi car gheta, tar ₹1.2 lakh down payment kara ani urlela amount 4 varshat repay kara. Yane tumcha EMI manageable rahto ani financial pressure kami hoto.

Benefits:

- Smart car buying decision: Tumhi tumchya budget pramane car select karta, emotional decision nahi gheta.

- Over spending control: High EMI mule future madhe problem yet nahi, unnecessary luxury avoid karta yeto.

- Loan burden manageable rahto: EMI low aslyane tumcha monthly cashflow stable rahto.

- Interest saving: Short tenure mule total interest kami bharava lagto.

- Financial stability: Tumhi savings ani investments continue thevu shakta, sagla paisa EMI madhe jat nahi.

Retirement Rules Explained (Example + Benefits)

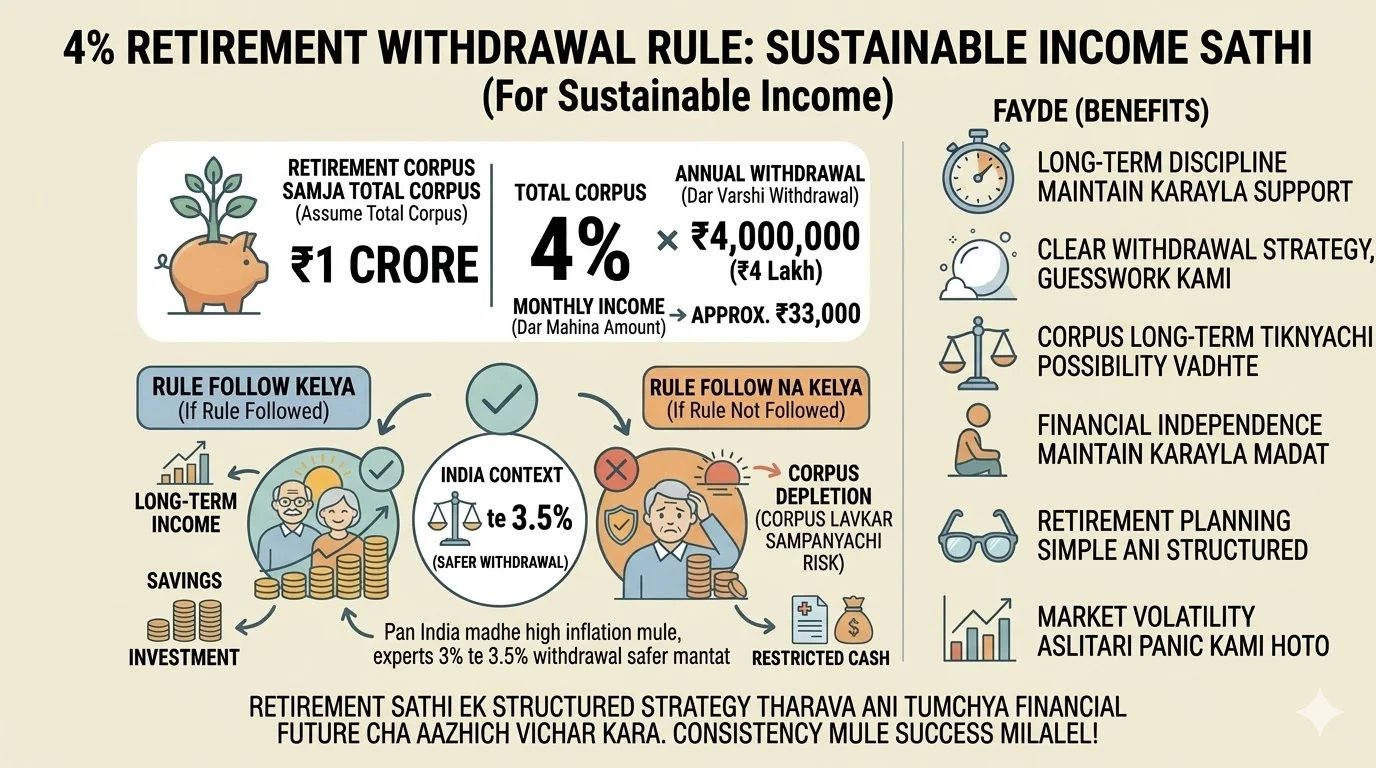

1) 4% Rule

4% rule ha ek simple pan powerful retirement planning tool aahe jo tumhala sangto ki tumhi tumchya total investment corpus madhun dar varshi kiti paisa safely withdraw karu shakta without corpus lavkar sampnyacha risk. Ha rule mainly long term sustainability sathi use hoto.

Basic logic asa aahe ki tumhi tumchya total retirement fund cha 4% pratyek varsha withdraw karu shakta ani urlela paisa market madhe invest rahato, jya mule to grow hot rahato ani inflation la beat karayla madat karto.

Example: Samja tumcha retirement corpus ₹1 crore aahe. Tar 4% rule pramane tumhi dar varshi ₹4 lakh withdraw karu shakta. Mhanje monthly approx ₹33,000 miltil. He amount tumcha basic expenses cover karayla use hoil.

Pan India madhe inflation ani medical cost jast aslyamule kahi experts 3% te 3.5% withdrawal safer mantat. Mhanun tumhi thoda conservative approach gheu shakta.

Benefits:

- Long term discipline maintain karayla support milto

- Clear withdrawal strategy milte, guesswork kami hoto

- Corpus long term tiknyachi possibility vadhte

- Financial independence maintain karayla madat hote

- Retirement planning simple ani structured hote

- Market volatility asel tari panic kami hoto

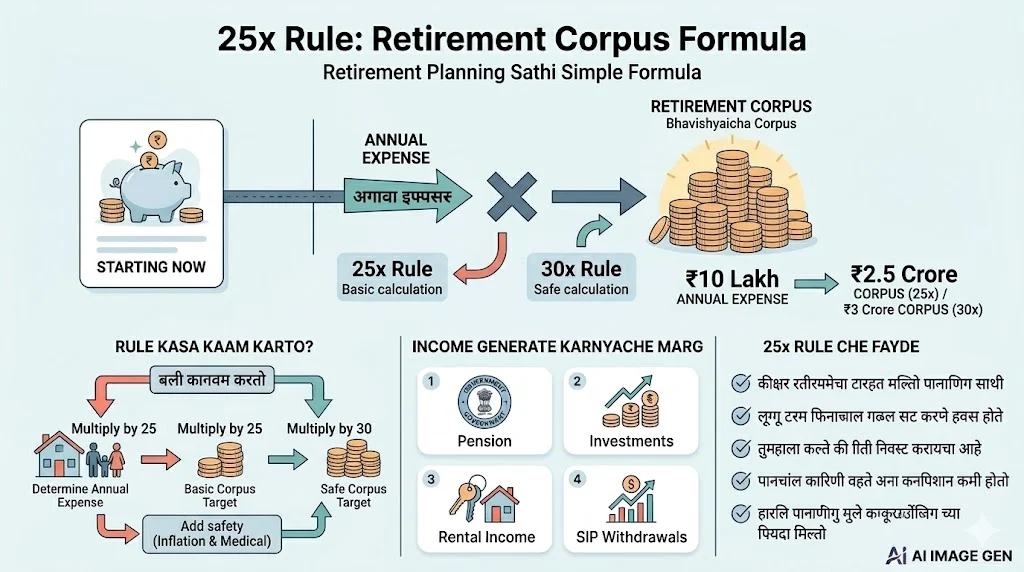

2) 25x Rule

Ha rule retirement corpus calculate karayla use hoto. He ek simple pan powerful formula aahe jo tumhala kalavto ki tumhala retirement sathi kiti paisa lagel. Ya rule nusar tumcha annual expense 25 ne multiply kela ki approximate retirement corpus milto. Pan India madhe inflation ani medical cost jast aslyamule 30x consider karne jast safe aahe.

Example:

Jar tumcha annual expense ₹10 lakh asel, tar basic calculation nusar ₹2.5 crore corpus pahije. Pan safe planning sathi ₹3 crore consider karne better aahe.

Benefits:

- Clear retirement target milto jyamule planning direction milte

- Long term financial goals set karne easy hote

- Tumhala kalte ki kiti invest karaycha aahe

- Financial clarity vadhte ani confusion kami hoto

- Early planning mule compounding cha fayda milto

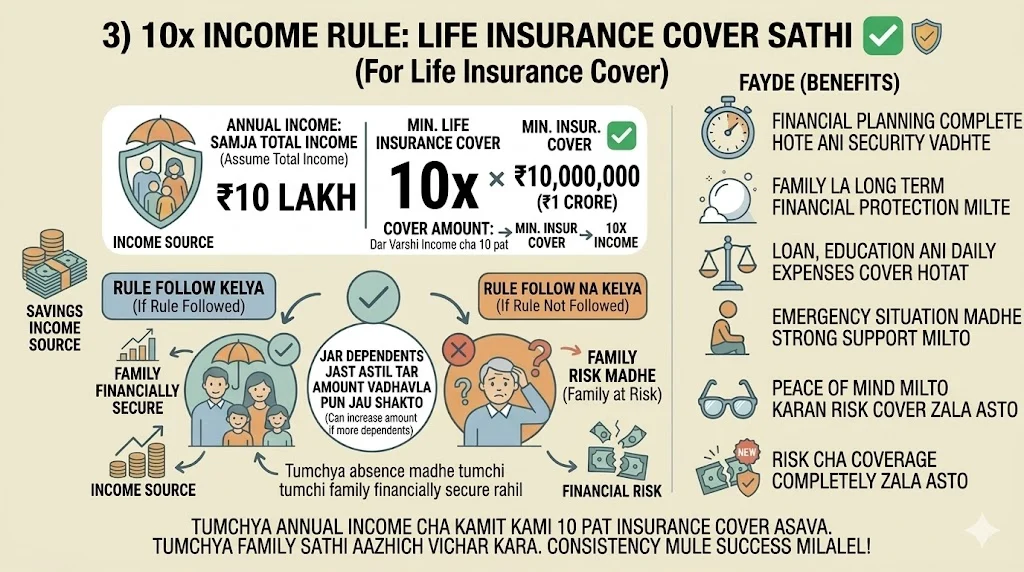

3) 10x Income Rule

Ha rule life insurance planning sathi use hoto. Ya rule nusar tumcha annual income cha kamit kami 10 pat insurance cover asava. He ensure karto ki tumchya absence madhe tumchi family financially secure rahil.

Example: Jar tumcha annual salary ₹10 lakh asel, tar tumcha life insurance cover kamit kami ₹1 crore asava. Jar tumchya var dependents jast astil tar he amount vadhavla pan jau shakto.

Benefits:

- Financial planning complete hote ani security vadhte

- Family la long term financial protection milte

- Loan, education ani daily expenses cover hotat

- Emergency situation madhe strong support milto

- Peace of mind milto karan risk cover zala asto

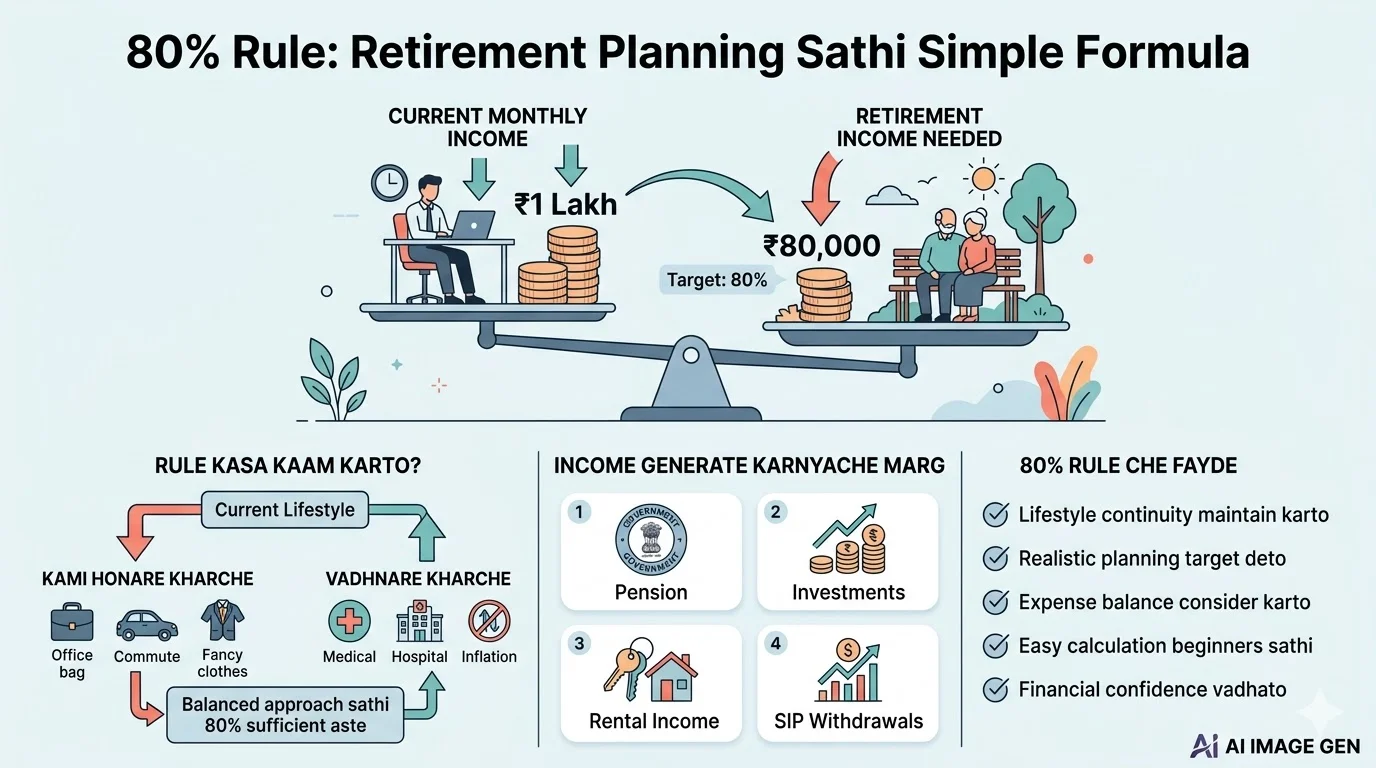

4) 80% Rule

80% Rule ha ek simple pan powerful concept aahe jo retirement planning madhe khup use hoto. Ya rule nusar, tumhala retirement nantar tumchya current income cha around 80% income pahije aste, jennekarun tumhi tumcha lifestyle maintain karu shakta. Retirement nantar kahi expenses kami hotat, jase ki office travel, daily commute, ani kahi lifestyle related kharche. Pan tyach veles medical expenses ani inflation mule kahi kharche vadhatat. Mhanun 100% income chi garaj naste, pan 80% income sufficient aste asa assume kela jato.

Example: Samja tumcha current monthly income ₹1 lakh aahe. Tar 80% Rule nusar tumhala retirement nantar ₹80,000 per month income pahije asel. He income tumhi pension, investments, rental income kiwa SIP withdrawals madhun generate karu shakta.

Benefits:

- Lifestyle continuity: Tumhi retirement nantar pan tumcha current lifestyle maintain karu shakta, jast compromise karava lagat nahi.

- Realistic planning: He rule tumhala ek clear target deto, jennekarun tumhi retirement corpus calculate karu shakta.

- Expense balance: He consider karto ki kahi kharche kami hotil ani kahi vadhatil, mhanun balanced approach milto.

- Easy calculation: Simple formula mule beginners sathi pan he samjun ghene easy aahe.

- Financial confidence: Tumhala kalte ki tumhi kiti saving karaychi aahe, mhanun future sathi confidence vadhato.

Final Thoughts – Real Rule Kay Aahe

Ek simple truth aahe: Personal finance is personal

- Tumcha income vegla aahe

- Tumcha lifestyle vegla aahe

- Tumche goals vegle aahet

Mhanun rules copy karu naka. Adapt kara. Jar tumhi he control kela:

- Budget

- Investing discipline

- Debt control

- Retirement planning

Tar tumhi already majority lokan peksha pudhe aahet. Baaki sagla noise aahe.

Related Posts :

Share This Post